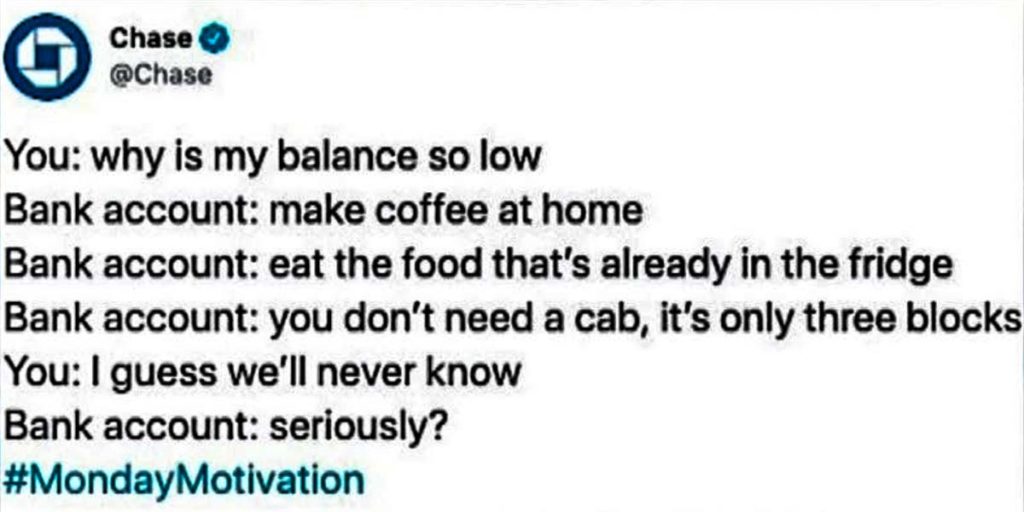

If you were wondering whether popular financial culture is lost in Wonderland, the backlash against Chase Bank’s tweet should clear that question up. Chase Bank highlighted the virtue of frugality, and the woke Twitterati were having none of it.

Here are a few reasons why the Twitterers are wrong.

Frugality is baked into the definition of building wealth

The formula for building wealth is spending less than you earn and investing the difference. There is no shortcut or alternate route around that.

The Chase tweet isn’t merely about making coffee at home or bringing a sack lunch to work as the reason why you might be broke. It’s about deliberate frugality in all of our financial dealings, from choices about minor expenses to major purchases.

The consumption culture lulls us into the sense that $5 purchases here and there are financially insignificant. The problem is that we are saturated in opportunities to spend small amounts of money in comparison to more frugal alternatives. These differences add up to enormous sums of lost wealth over our lifetimes.

That extra channel package or internet bandwidth increase is just $14. That extra 100 square feet of apartment living space is just another $140 per month. The authentic new purse at Neiman Marcus is only $140 more than the indistinguishable knock-off on Amazon. The new camera is only $1,400 more than the used one. The new truck is only $14,000 more than the previous model. The new-construction house is only $140,000 more than the older one down the street.

Over a lifetime, those small decisions are the difference between building wealth and reaching financial independence or spending your golden years scratching out a living on social security.

Financial habits determine your financial destiny

Bank employees learn through observation the financial habits that lead to a growing bank account. They also see which ones mire people in perpetually low balances. Chase’s advice should be heard as a needed reminder, not a dumping ground for woke indignation.

My early twenty-something years were spent working at credit unions, and I couldn’t tell you how many times people came in requesting loans for stuff that was beyond their means, even people with stratospheric incomes.

One example was a specialty loan for the $35,000 membership fee at the local university’s golf course. Anesthesiologists, presidents of the college, top coaching staff, and business owners making $400k per year would apply for those loans, unable to pay the fee out of their own savings. Some of them would even get turned down for the loan.

Why?

Despite making $35k or more per month, they didn’t even have that much saved in a bank account, accessible for borrowing from a 401k or selling from a taxable investment account, or available on their $100k limit credit cards. They spent every dime they earned, never building wealth and always swimming in debt.

That’s why I cringe when people say, “I can’t get ahead because I’m not paid enough.”

Plenty of those same people would spend hundreds of dollars on entertainment over a weekend, overdraft their accounts, and then come into the credit union on Monday and blame overdraft fees, credit union “greed,” the the employees of the non-profit themselves for their problems in life.

The gig economy people who have $1,000 iPhones, no savings, and complained about overdraft fees are the same as the $400,000 per year anesthesiologists that have no savings and were denied $35,000 golf course membership loans.

If you don’t have frugality firmly ingrained in your behavior, then you will never build wealth, no matter how much or little you earn.

You are responsible for your own financial future

Here are a few common critiques against Chase. See if you can spot the common themes:

- Because Chase was bailed out with $25b in TARP funds.

- Because Chase charges a monthly fee for services.

- Because of systemic systems of institutionalized oppression.

- Because employers don’t pay living wages.

- Because I have to pay student loans.

- Because I had to pay rent.

- Because I earn gig wages.

The problem with the criticism of Chase’s tweet is that it’s rooted in the mentality that it’s someone else’s fault why I can’t get ahead.

None of the above listed critiques are Chase’s problem, and casting yourself as a helpless victim in a sea of overwhelming challenges won’t help.

You choose where you bank. You choose to pursue an unbelievably expensive and useless degree. You choose not to downsize or live with a roommate to cut your housing costs. You choose whether or not you will work towards higher-paying employment.

Are you a liberal arts grad paying student loans and making $15 an hour in the gig economy? If you have a $6 coffee in one hand and a $1,000 phone in the other, then you should pay attention to Chase’s advice.

Whatever hole you find yourself in, frugality is the first step towards digging yourself out. Switch to a credit union that doesn’t charge a monthly fee. Work more hours, pay off your loans, and don’t let your kids make the same mistake. Set your ego aside and live in cheaper housing. Get a roommate. The average life expectancy is 78 years. Don’t tell me you can’t improve your skills and find better employment in that amount of time.

You don’t have a better strategy

You must take responsibility for your economic situation because you don’t have a better strategy for building wealth and you never will. Your best bet is to play the hand you were dealt in life as best as you can play it. No matter what your hand looks like, following Chase’s frugality advice will make it financially stronger.