Keep a personal balance sheet to make sure you’re headed in the right financial direction. Photo by Pavel Kunitsky, CC0

Do you have any idea what you’re worth? How about this – do you know whether or not you are on a financial trajectory to get you to the level of wealth you want to achieve by the age you want to achieve it?

Many people not only answer “no” to both of these questions, but they are in a position of worse than just a “no” answer in that they don’t know how to get from “no” to a “yes” answer. But if you want to hit your wealth goals, you need to have a “come to Jesus” moment with your finances, and I’ll show you how.

Want to know what is the most important habit I’ve discovered that has continuously moved me in the direction of increasing my wealth?

Opening a now 10-year old Excel document every month and updating my personal financial statement.

Take an Idea from the Corporate World

In the corporate world, there are two important documents that help owners and shareholders determine the financial strength of a company. The first type of document is called a balance sheet. The balance sheet shows what the business is worth, what revenue to expect in the near future, what expenses must be paid, a list of assets and liabilities, whether the company can likely qualify for credit, and other metrics. The balance sheet helps to uncover problems and give direction to actions that need to be taken to improve the financial standing of a company.

The second important document is a cash flow statement. This statement shows all of the sources of income for a company as well as all of its expenses. It is broken down into three categories: operations, investing, and financing. It lets company managers know whether the company is currently sinking or swimming.

What do these two documents, that together are part of a broader financial statement, have to do with you?

The Personal Financial Statement

I’m not sure where I got the idea from, but when I graduated from college I adopted the habit of keeping a monthly Excel spreadsheet of my personal financial statement. It tracked my monthly sources of income, expenses, assets, and liabilities. Off to the right side of the sheet was a column of the months in the year. I would write my net worth and net liabilities next to each passing month as time went on.

Every December, I would highlight the entire sheet, copy it, and paste it into a new tab within the same Excel document. I’d title this new sheet and tab with the current year. The old sheets were kept in their respective tabs at the bottom of the document. These past years’ tabs and sheets formed a growing personal financial history as well as a neat little history of my life.

As the years went by, I came to realize the importance of this habit. This living financial statement continually kept me honest about reaching the financial goals I had set for myself. It ruthlessly pointed out my career and investment shortcomings and gave me direction on what changes I had to make to reach the financial goals I set for myself.

Because of this constant recognition of where I stood financially, I was able to make informed decisions about career changes, investment choices, and how to best deal with paying down student loans and other debts.

It doesn’t matter how old you currently are or what your financial situation is; if you want to be wealthy, or at least wealthier, you have to make a habit of knowing your worth and determining whether you are on track to meet your wealth goals. Obviously the younger you are when you start this habit the better. I wish I had started tracking my finances in middle school because I know I squandered lawn-mowing money that a personal balance sheet would have encouraged me to invest instead. So if you’re in grade school reading this article, it’s for you, too, so pay attention. Time is on your side in a BIG financial way. Take advantage of it!

Let’s Get You Started

There are many places and document formats you can track your net worth on, but Excel has been around since forever and it’s not going anywhere soon. Even if it does, an Excel document is easily convertible into whatever new format comes out, like Google Sheets (which is what I converted to and currently use). So open yourself either a new spreadsheet, Excel or Docs or whatever you prefer. I’d avoid using a proprietary program as you never know when these will be suddenly discontinued or fall from favor. Name the document “Balance Sheet” and name the first tab at the bottom the current calendar year.

What Goes on the Sheet

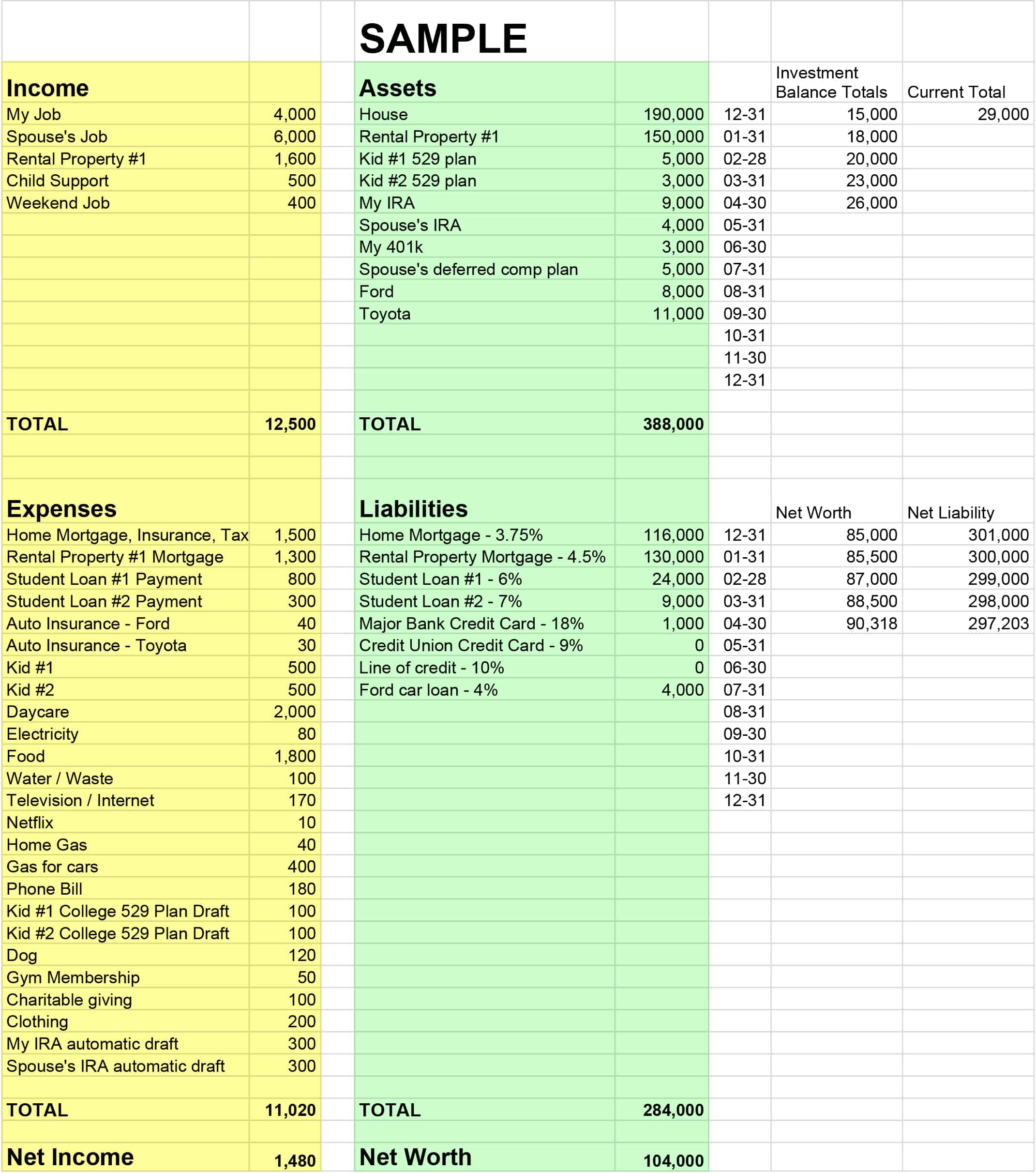

So what should you include in your personal financial statement? There are largely two things at a minimum you should track: 1. income and expenses and 2. assets and liabilities. Here’s a sample of how you can organize your spreadsheet:

Sample Personal Financial Sheet

Yours may be more or less complicated than the example shown, but the structure should be roughly the same. Just shape the details to your particular situation. Include every little source of income and expense that you can think of. If you’re not sure how much you spend on food or clothing or other fluctuating and recurring costs, start paying attention to those expenses and come up with an average. I always purchase gas with the same credit card, so I can take a 6 month period on my credit card statement, search for gas purchases, and figure out what my average monthly gas expense is. Do that with every variable expense you have so you’ll end up with an accurate spreadsheet.

Under the assets column, only list assets that are commonly marketable or are actual investments, such as any real estate you own, stocks and bonds, cars, or other major assets. Appraise things conservatively. Don’t bother listing jewelry or electronics or collectibles – those are not investments. If you find that everything of value you own is in baseball cards or computer parts or camera gear, then having nothing to show under the assets column is a good first lesson this sheet will teach you. The value of collectibles – your grandma’s earrings, a painting you bought from an up-and-coming artist, some old baseball cards – can change without warning and cannot be relied upon to build long-term, cold, hard wealth.

Under the liabilities column, list any credit cards, mortgages, car loans, open lines of credit, student loans, or other debts you have. It’s useful to list the respective interest rate next to each source of debt. That way you are constantly reminded of which debts you should be paying down first. It’s difficult to make an extra $200 principal payment on a 4% rate car loan when you have a $200 balance on a 16% rate credit card.

Somewhere on you sheet, have a column of months of the year. As each month goes by, list your net worth and your net liabilities. Study the trends of these numbers as the months go by. You should feel motivated to see your net worth go up and your liabilities go down. If the opposite is occurring, then start making changes in your life to get the numbers going in the right direction.

Going Forward

Want to join the ranks of the wealthy? If you have done what I illustrated above, then congratulations, you are on the right track. You now have a point of reference to look at and determine what financial steps you should take next. Now, depending on what level of wealth you want to achieve, it’s just a matter of making the changes needed to get you there: open your own business, start a new career, increase your monthly investments, pay off debt, etc.

Make a habit of keeping up with this spreadsheet once a month and you’ll empower yourself to constantly move towards your goals.